Navigating the "Higher-for-Longer" Housing Market: What Today’s Inflation Means for You

Before the headlines send anyone into a panic, let’s unpack what is actually going on with the economy, why it is driving mortgage rates, and what it really means if you are looking to buy or sell a home right now.

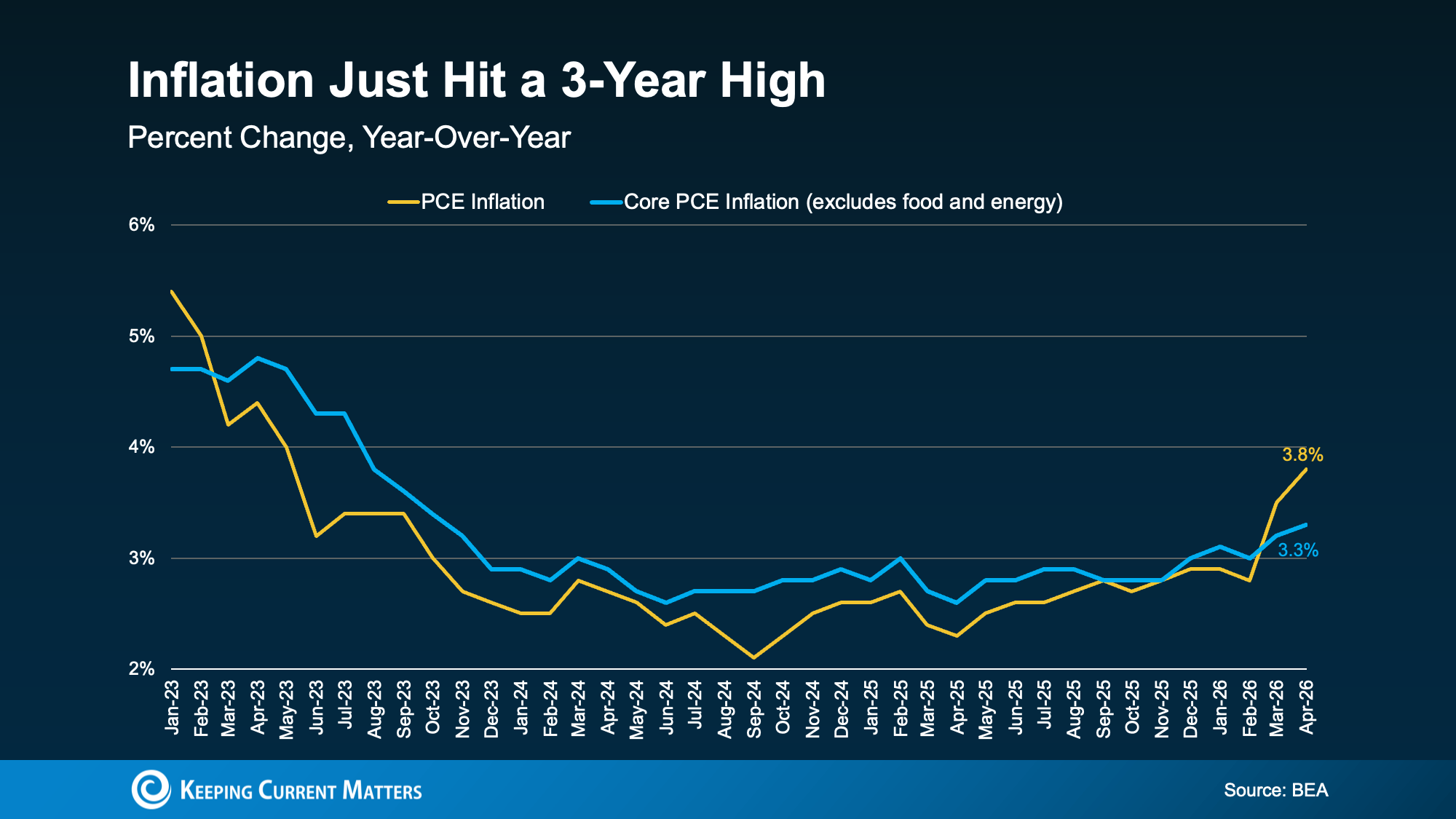

Inflation Went Up – Here’s What That Means

The government tracks inflation in a variety of ways. One of the most important metrics is the Personal Consumption Expenditures (PCE) Price Index. It measures how much more (or less) people are paying for everyday goods and services compared to a year ago.

There are two versions of this index that economists watch:

Headline PCE: This is the overall number you see in the news. It has shown recent spikes, driven heavily by global conflicts pushing gas and energy prices higher.

Core PCE: This is the exact same measure, but with volatile gas and energy prices stripped out.

The Federal Reserve (the Fed) watches the Core PCE number most closely because energy prices swing wildly and can distort the true trend. Core PCE is rising, but not nearly as fast as the headline number. This suggests a good chunk of the inflation pressure is tied directly to international energy disruptions. When those situations eventually settle, inflation should follow suit.

Why This Matters for Mortgage Rates

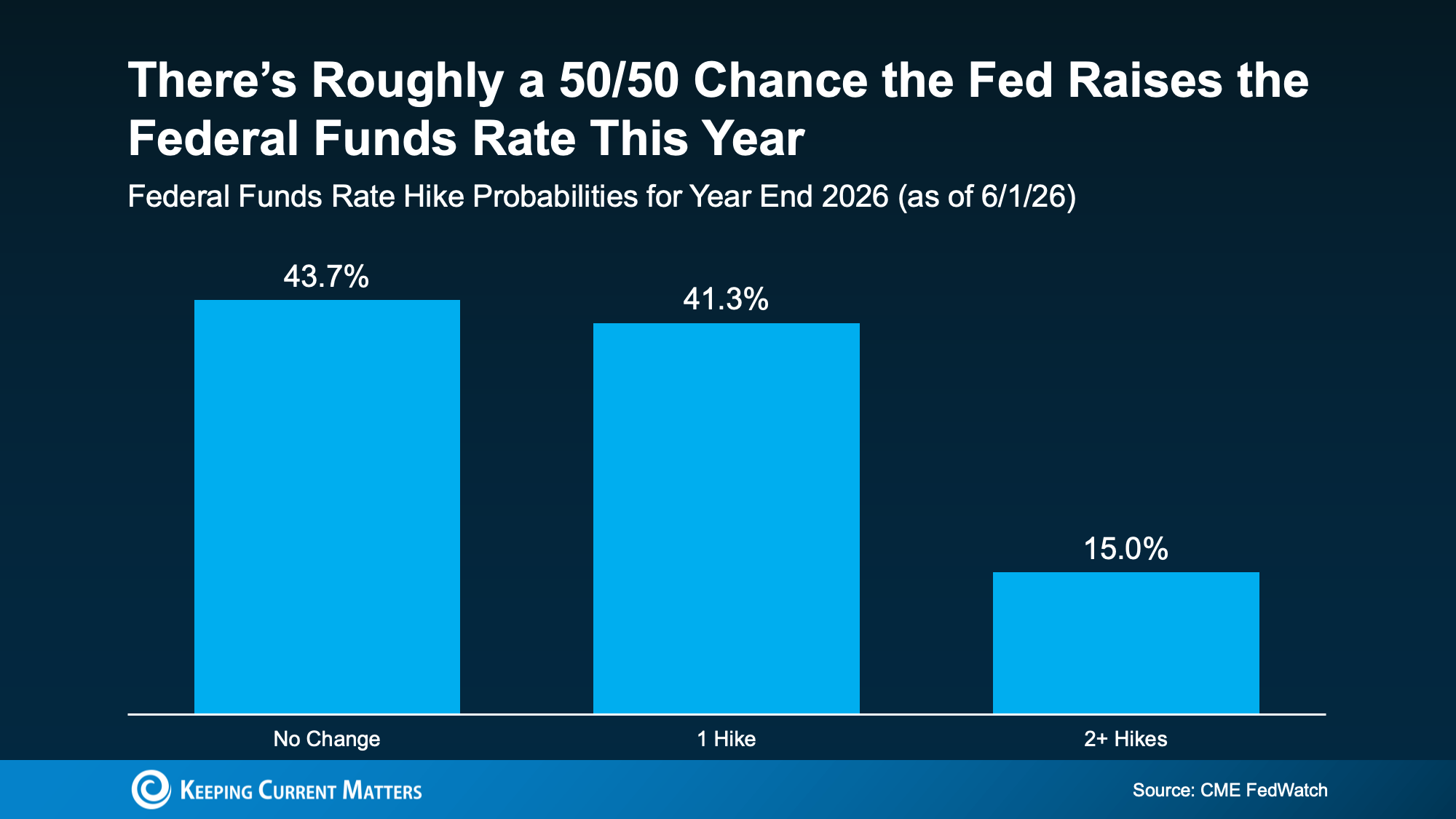

When inflation remains stubborn, the Fed keeps its benchmark interest rate elevated to cool down spending. While the Fed doesn’t set mortgage rates directly, mortgage rates generally trend in the same direction as the Fed's policy outlook.

Current data from the CME FedWatch tool shows that the market expects the Fed to hold rates steady for the immediate future. This means mortgage rates are not likely to drop significantly anytime soon. If you have been waiting on the sidelines for rates to fall back to recent lows before making a move, "higher for longer" is the reality of the current economic landscape.

As noted in recent market analysis by Bankrate:

"Oil prices and bond yields have dropped a bit . . . but they're still way up compared to the start of spring. Until there's a resolution to the war, look for both inflation and mortgage rates to stay high."

But This Is Not 2008 – Not Even Close

A challenging, high-rate economy does not mean a housing crash is on the horizon. The structural foundation of the housing market today is fundamentally different from what led to the 2008 collapse:

Low Inventory: There is no massive flood of homes hitting the market. Supply remains relatively tight.

Strong Equity: Most homeowners today have a significant amount of equity built up in their properties, preventing widespread default risks.

Strict Lending Standards: Getting a mortgage requires rigorous financial verification today, unlike the loose lending practices of the mid-2000s.

Today's challenge is strictly about housing affordability, not a wave of distressed, underwater sellers. The market feels heavy and slow, but a hard market is very different from a crashing market.

You Still Have Options: Strategies for Buyers and Sellers

High rates do not mean your real estate goals have to stop. It just means your approach needs to adjust to the current terrain. Real strategies are moving deals forward every day:

Explore Alternative Loan Options: Ask a lender about adjustable-rate mortgages (ARMs), which offer lower initial rates, or temporary rate buydowns (like a 2-1 buydown) where the seller pays to lower your interest rate for the first couple of years.

Leverage Seller Concessions: Because buyers face higher costs, many sellers are willing to offer credits at closing to cover down payment assistance or interest rate reductions instead of just dropping the purchase price.

Focus on Lifestyle Over Timing: Trying to perfectly time the market is a losing game. The right strategy, tailored to your specific financial situation, matters far more than waiting for a perfect interest rate that may take years to arrive.

Bottom Line

Inflation is proving to be sticky, and that means mortgage rates are likely to stay elevated for a while. But for people who need to move, success comes down to custom strategy, not market timing.

Wondering how these economic shifts impact your specific real estate goals or neighborhood numbers? Connect with a trusted local agent or lender to build a plan that works for you.